SHARES ADDED

- Thong Guan @ RM2.60

- MagniTech @ RM1.93 @ RM1.97 @ RM1.99

- ATRIUM @ RM1.47

- FAVCO @ RM2.50 @ RM2.55

- KAWAN @ RM1.67

PACKAGING

BPPLAS profit improved QoQ and YoY. Share price increase 13%. Thong Guan on the other hand dropped to -5%. The Q4 result from Thong Guan is yet to release.

FURNITURE

LiiHen annouced 3.5 cent dividen. Q4 profit improved by 165% compared to Q3. The worst is probably over but still have issue like labour, resin cost and high shipment cost. Pohuat is flat but notably investment guru, COLD EYE has emerged as top 30 shareholders. It is good time to add Pohuat!

PLANTATION

Both INNOPRISE and HSPlant are star performers this month. Superb profit and revenue due to high CPO price. HSPlant announced 15.5 cent dividen and share price spike to RM2.89 with an appreciation of 50%. INNOPRISE announced 6 cent dividen and share price rocketed to RM 2.01 with an appreciation of 72%.

I dispose all HSPLAN share and two third of INNOPRISE shares. Capturing profit of 35% for HSPLANT and average of 52% for INNOPRISE.

Lesson to be learned here is to capturing maximum profit. So timing is important. Usually share price will soar for few days or weeks if all sentiments are good.

OTHER

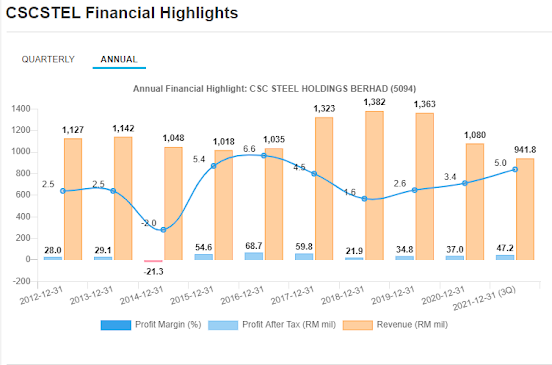

SamChem and CSC Steel perform well. Share price improved by 19% and 18% respectively. Both counters registered profit improvement on Q4. CSCSteel declared 14 cents dividen, higher than expected. Samchem declared 1.5 cent. Proft taking activity took place at RM1.00. However, SamChem is good for long term growth and may accumalate when price drop below RM0.90.

New kids on the block are FAVCO and KAWAN. FAVCO has announced 8 cents ( a bit disappointed). KAWAN Q4 result is yet to release.

FINANCE

No surprise from finance sector except better result in Takaful. RCE and ELK-DESA are flat.