Company : RCE Capital Berhad

Business :

Money

lending (personal financing) to government servants. A subsidiary of Amcorp Group. This

is good business as payment is very secured (direct debit from salary). The profit margin is a whopping 45% !! Mana cari this kind business model?

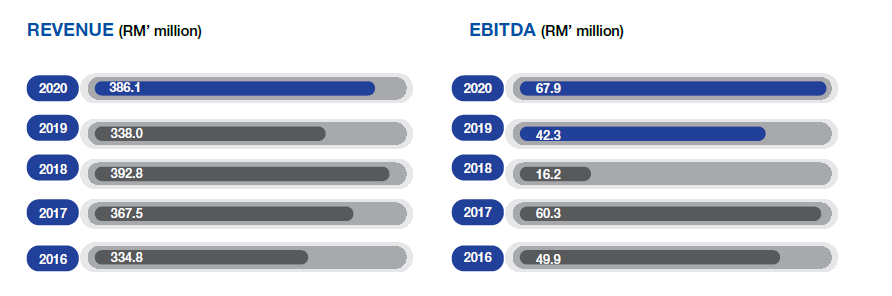

Q4 Result

Consistence

revenue and profit for FY 2021. Hopefully they can maintain RM34 million profit

every quarter throughout FY 2022.

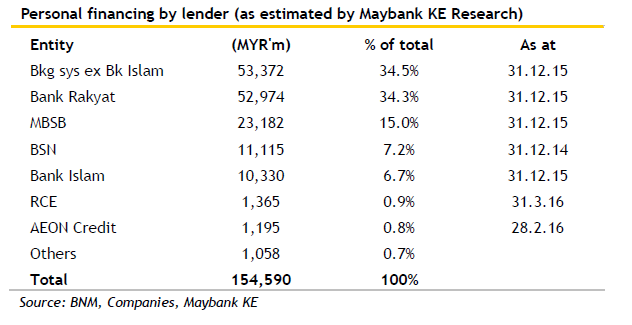

The write-up by Maybank Investment bank (sometime ago) is very interesting. RCE Cap has a very similar business model to AEON Credit.

Prospect:

They

are bidding for digital banking license with a consortium together with Star

Media Group and Paramount Corp but I think chances are low. The low interest

environment is good for RCE as it brings down their cost of funds. See below.

Malaysia

emoluments for Government sector is growing every year and this bode well for RCE business. See chart below.

My

view on share price:

Price

has risen from mid Nov 2020 to all time of RM3.00 around June 2021. It is then

dropped to current price of RM2.74. The support level is around RM2.55-RM2.60 and

this is a good entry if you wish to buy some.

Dividen

payout is pretty consistence and increasing every year from 2017. Forecast for

FY 22 will be 14 cents.

Forecast earning & PE.

Current PE is 8.5 at RM2.74 (23 July 2021) and forecast EPS for FY2022 is 37 cents. So fair value should be RM 3.14 ! The coming Q1 result is very important indicator for FY2022 share price.

|

Q1 |

Q2 |

Q3 |

Q4 |

Total |

|

9.0 |

9.0 |

9.5 |

9.5 |

37 |

This

is one of the companies that invested by famous local investor, Cold Eye (I

read most of his books). At time of

writing, I own RCE Capital shares for some time and will continue to keep till maximum appreciation.