Business

:

Manufacturing

of various drinks such as Alicafe, Warung, Ah Huat Coffee and export to

oversea market especially to MENA/Gulf Region. Their products cover all

consumers in Malaysia. See images below. I like their P.Ramlee ads in Youtube 😊

Net

cash company again with RM110 million cash and RM7.8 million bank borrowing. So

no problem to weather through difficult times. See their 2020 annual report

below:

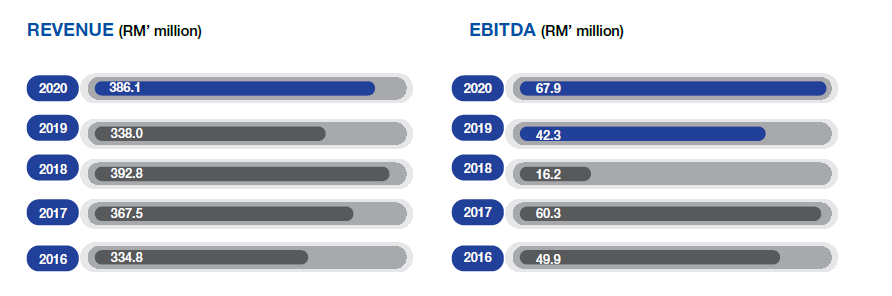

5

years revenue

The 5

year revenue track record is as per chart below. Year 2020 was a record profit

for the company but 2018 was low. The 2018 annual report said that low profit

was due to write down of inventories and PPE.

Export business:

The

main export market is MENA. In fact, it is heavily depending on MENA region. No

information of the revenue breakdown for China and Singapore. See their latest quarter result below.

Q4

Result

There was a huge drop in profit in Q4 due to lower sales and higher write-down. If you see the profit chart above, you will notice profit has been dropping on every quarter for FY 2021. Can it recover? Time will tell.

However, cash flow from operation is still very healthy. RM26 million has been used for investment of plant property and equipment so the cash has dropped to RM86 million. See their cash flow statement in Q4 report.

Few

positive news on the company as follow:

- Company will launch new product “Frenche Roast”

for people with more sophisticated taste such as Caramel Latte, Tiramisu

Latte and French Latte.

- They have added two filing machines to increase

the annual output. See note below.

Risk

Following

are the risks that may cause sales and profit drop:

- Sugar tax hike in key markets of UAE and KSA.

- Raw material price of sugar increase.

- Packaging material price increase (both plastic and aluminium can)

- Coffee bean price increase

- Shut down of plant due to COVID cases (export shipment will be delayed).

Major portion of the raw material cost are sugar (25%) and packaging (15%).

Not very optimistic that profit in coming quarters will be good. KWAP has been disposing the shares for sometime and also take note that one of the founders, Dato Low Chee Yen passed away. He was instrumental in developing the company. Can Wang Tak Keong leads the company out of blue? Time will tell but he keeps selling the warrants!!

My view on share price:

Price

drop from peak RM2.60 till RM.130, almost 50% drop! Near term will not recovered so soon. Probably will take 3-4 quarters time to get back to normal.

Forecast earning & PE.

In terms of earning, if they don’t going into lost then considered very good. Just simple forecast of 2.4 eps and PE will be 50 at RM1.33 which is high and there is room for price to drop further.

|

Q1 |

Q2 |

Q3 |

Q4 |

Total |

|

0.4 |

0.5 |

0.5 |

1 |

2.4 |

However, company is very generous in dividen. They will pay minimum 50% of the profit and on every quarter. So definitely a good dividen company.

At time of writing, I do not own any Power Root shares.

👍🏻💪🏻

ReplyDelete