Company : BPPlas Berhad

Business :

Manufacturing PE stretch film in Batu Pahat Johor. The profit margin for plastic is usually single digit (except SLP, SCGM). This business is largely depending on raw material (resin) cost. Stretch film usually use LLDPE (liner low density Polyethylene) as raw material.

Side

note:

The

local supplier for PE (including HDPE, LDPE & LLDPE) is Lotte Titan

Chemical based in Pasir Gudang (another public listed company in Malaysia). More

information of usage of PE can be found via link below:

https://www.lottechem.my/products/productGuide_view.asp

Fundamental

:

Net

cash company and consistently giving out dividen every

quarter. It is perfect choice for those who seek high dividen yield and

consistent dividen payment. The company has increased their cash to RM84 million

(2020) compared to RM45 million in 2019. Well done management and board of

directors!

5 years revenue is pretty flat or consistence. See below.

Export is 70% of their business which can benefit from high USD/RM exchange rate.

Recently

BPPlas has released their Q1 result and performance is very encouraging. In

fact one of the highest revenues and net profits. Profit margin also

increase to 9.7%! See chart below.

BPPlas

- Q1 Result

I

include other plastic companies latest QR results for comparison purpose except

Scientex (they have property business).

SLP - Q1 Result

Thong

Guan Q1 Result

SCGM

Q3 Result

Daibochi

- Q2 result

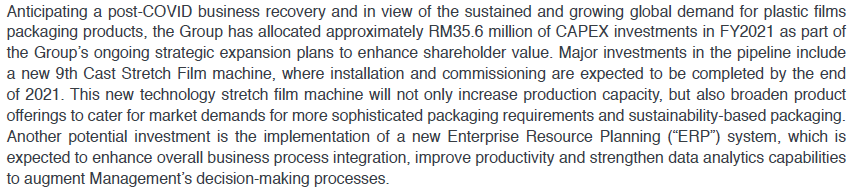

Prospect:

Resin

price is the key factor for profitability. If they can pass the cost to end

users/customers then profit should be good. The e-commerce logistic is a

booming sector. Hopefully they can capture this opportunity. Growth wise is not

very aggressive but they will invest in new machine. This will only contribute

to the earning in 2022 as installation and commissioning will long time

(typically 1.5 years).

![]()

Company will invest in new machine. Good sign.

Raw material

/ Resin price:

The

resin price shot up in Mar and then slowly soften in May (see resin chart below).

Coming Q2 result will be lower profit as I don’t expect the company can pass on

the resin cost so quickly. Long term prospect is considered OK as still lower

than average of 9200 in 2018 (see resin chart below).

My

view on share price:

This

company is a bit like old man (ah Pek) company. Website show very little information on

their product usage. The price can stagnant for a long period of time. If you

look at the price chart, share price can hibernate (price flat) for whole year 2019

and again 4 months in 2021 except the recovery from Covid sell down in Mar

2020.

Simple

2021 EPS forecast will be 5x3 + 4 = 19 cent. At price of RM1.60, the PE will be

8.42 which is low when compared to others but it is always hovering around 8-9

most of the time. I don’t think it will increase to PE 15 as lack of

institution coverage or “goreng”. Factor in a small growth, it is possible to

appreciate until RM1.80 based on PE 9.5. However, the peak price was around

RM1.73 and seems hard to break RM1.80.

I do not expect the share price to fly in coming months (old already!) but company is stable in giving dividen. Suitable for low risk appetite investors. See note below.

At time of writing, I own few BPPlas shares…support old man a bit lah, better than bank FD rate! 😊

No comments:

Post a Comment